How to build a retirement portfolio in India

How to Build a Retirement Portfolio in India: A Complete Guide , IndianRetirement-the term sounds soothing to some, intimidating to others. For most Indians, it more often means a mix of emotions: freedom from work and appraisal pressure versus worries about how to manage expenses that were hitherto being supported by the regular flow of income. But here’s the fact: retirement actually can be one of the most beautiful and stress-free phases of life-if planned wisely.

The motive behind this blog is to explain how one should create a retirement portfolio in India in a somewhat simple and workable fashion that every individual will understand, even if one has just started investing.

Table of Contents

Toggle1. Understand what a retirement portfolio is

A retirement portfolio is not one investment, but several savings and investments put together which will help meet his or her needs once he or she stops working.

Think of it as a ‘thali’: you need rice, dal, sabzi, roti—a bit of everything to make it complete and wholesome. Likewise, different investments complete your mix in your portfolio.

2. Savings could be initiated with less money as well

Probably the biggest mistake most Indians make is that they start off very late. Often we say to ourselves, “Let me earn a bit more first,” or “I’ll start saving next year.” But when it comes to retirement, time becomes your best friend.

In fact, even a regular investment of ₹1,000 or ₹2,000 a month in your 20s or 30s will turn into lakhs by the time you retire. That’s the magic of compounding: your money earns interest, and then that interest earns more interest.

Example:

Investing ₹ 5,000 per month for 30 years at a return of 10% will see the amount rise to nearly ₹1.13 crore.

If you waited 10 years and started at 40, you get about ₹ 37 lakh only.

Moral: Start early, start small – but sta

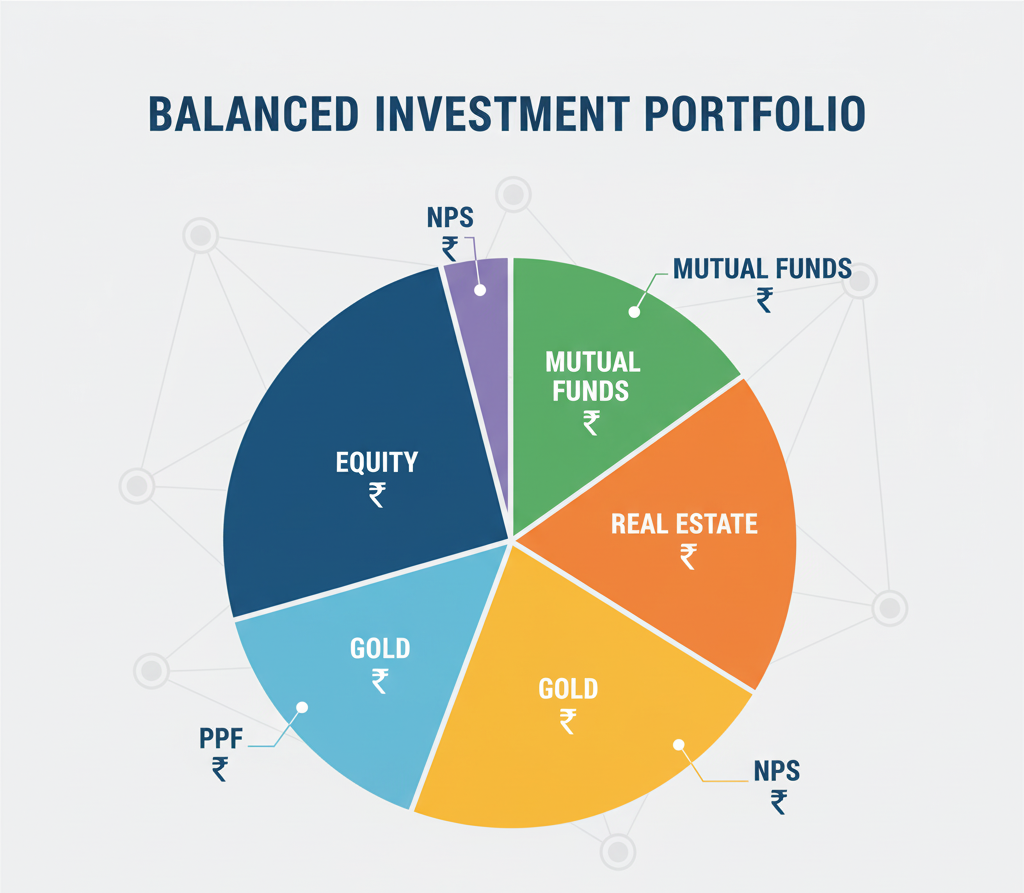

3. Diversify Your Portfolio — Do not place all your eggs in one basket.

Your retirement portfolio should have a different class of assets that balances risk and return.

This means the following to an Indian investor:

Equities are investments in stocks, mutual funds among others.

These yield higher returns but are risky too. You could invest in index funds or diversified mutual funds for long-term growth.

Yellow: Debt – Bonds, PPF, EPF, NPS

These give stability. Products like Public Provident Fund, Employees’ Provident Fund, or National Pension System are great for the long term.

Gold :

Gold has an emotional value amongst Indians. It also serves as an hedge against inflation. You could consider the SGBs as a substitute for physical gold.

⚪ Real Estate:

A house to stay in is good, but don’t overinvest in it. Property gives security, but it is not readily saleable when you need money.

Cash & Emergency Fund:

Contingencies: Always maintain at least 6 months of expenses in your savings account or liquid fund for contingencies.

4. Introduce smart tax-benefit schemes.

A few tax-saving and retirement-friendly options have been given by the Indian government.

EPF: To be deducted at source.

PPF: Safety and long-term options, returns are tax-free.

NPS: Additional tax deduction up to ₹ 50,000 under section 80CCD.

SCSS stands for Senior Citizens Savings Scheme. It is ideal once you retire.

Understanding these and using them smartly will not only help in saving on taxes but also help in building a stable retirement base.

5. Rebalance as You Age

You can take more risk when you are younger, meaning investing more in equity, while you should gradually shift to safer investments as you approach your retirement. A simple thumb rule: Equity %= 100 – Your Age Thus, if you are 30 years old → 70% in equity, 30% in debt. If you are 55 → 45% equity, 55% debt. This means with time, your portfolio automatically becomes safer.

6. Think Beyond Money:

Plan for Lifestyle It is not all about the money in retirement but how you want to live. Can you see yourself traveling, living in a quiet town, helping out your grandkids? The amount you save is a function of your lifestyle goals. Take time to visualize it, really-think of the perfect retirement. It will be your motivator that will enable you to stay with the plan.

7. Don’t Forget About

Inflation Everything keeps increasing in price. ₹1 lakh today won’t have the same value after 20 years. This means your investments must be growing faster than inflation. Equity and NPS, in the long run, would help one beat inflation, so they need to be part of your retirement planning.

8. Review Once a Year Markets change.

Life changes. So once a year, sit down with your numbers: Check if your investments are on track. Increase the SIP amount as your income increases. Shift funds from high-risk to low-risk options if nearing retirement age. A yearly one-day check will save you from years of stress later on.

9. Consider a Financial Advisor

The final point to remember is that if you’re confused or not comfortable doing the money management yourself, that’s totally okay; get some help. A certified financial planner can help an individual create a portfolio based on his goals, age, and income. Think of it as hiring a fitness trainer-it’s worth it if it keeps you disciplined.

10. Be consistent, be patient.

The single most powerful tool in building wealth is discipline. When markets go down, do not stop your SIPs. They average out and grow over time. Retirement planning isn’t a sprint-it’s a marathon. Final Thoughts Building a retirement portfolio in India isn’t about being rich; actually, it’s all about being ready. Whether you are 25 or 45, the best time to start is now. Take small sure steps and make smart choices, and you can make your golden years really golden: peaceful, independent, and full of joy.